Despite being months behind, many strapped residents are hanging on to their homes, essentially living rent-free. Pressure on banks to modify loans and a glut of inventory are driving the trend.

Patricia and Eugene Harrison, who bought their Perris home seven years ago, have lived there since October 2008 without making any payments on their mortgage. ( Irfan Khan / Los Angeles Times / February 19 , 2010) |

By Alana Semuels

February 27, 2010

It's been 16 months since Eugene and Patricia Harrison last paid the mortgage on their Perris home. Eleven months since the notice got slapped on their front door, warning that it would be sold at auction.

A terse letter from a lawyer came eight months ago, telling them that their lender now owned the house. Three months later, the bank told them to pay up or get out by the end of the week.

Still, they remain in the yellow ranch-style home they bought seven years ago for $128,000, with its views of the San Jacinto Mountains. They're not planning on going anywhere.

"We're kind of on pins and needles, but who'd want to leave when you put this kind of energy into a house?" said Eugene Harrison, 70, gesturing toward a bucolic mural of mountains, stream and flowers the couple painted on the living room wall.

Throughout the country, people continue to default on their home loans -- but lenders have backed off on forced evictions, allowing many to remain in their homes, essentially rent-free.

Several factors are driving the trend, industry experts say, including government pressure on banks to modify loans and keep people in their homes.

And with a glut of inventory in places like Southern California's Inland Empire, Nevada and Arizona, lenders are loath to depress housing prices further by dumping more properties into a weak market.

Finally, allowing borrowers to stay in their homes helps protect the bank's investment as it negotiates with the homeowners, said Gary Kirshner, a spokesman for Chase bank, a major lender.

"If the person's in the property, there's less chance for vandalism, and they're probably maintaining the house," he said.

Economists say the situation won't last forever, but in the meantime the "amnesty" may allow at least some homeowners to regain their financial footing and avoid eviction.

In the Inland Empire, an estimated 100,000 homeowners are living rent-free, according to economist John Husing, who based that number on the difference between loan delinquencies and foreclosures. Industry experts say it's difficult to say how many families are in that situation nationally because only banks know for sure how many customers have stopped paying entirely.

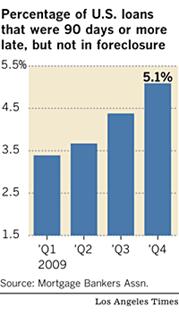

But Rick Sharga of Irvine data tracker RealtyTrac notes that the number of loans in which the borrower hasn't made a payment in 90 days or more but is not in foreclosure is at 5.1% nationally, a record high. And yet the number of foreclosures last year was 2.9 million, below the 3.2 million that RealtyTrac economists predicted.

More evidence is provided by another firm, ForeclosureRadar, which says it now takes an average of 229 days for a bank to foreclose on a home in California after sending a notice of default, up from 146 days in August 2008.

"For some reason, banks are being more lenient with homeowners who are behind on their loans," Sharga said. "Whether it's a strategy to try and slow down the volume of foreclosures or simply a matter of the banks being able to keep up with volume is something that banks only know for sure."

Lenders say the trend reflects their efforts to work with borrowers to modify loans to avoid foreclosure. Bank of America "continues to exhaust every possible option to qualify customers for modification or other solutions," spokeswoman Jumana Bauwens said.

Some lenders are making it a policy to partner with delinquent borrowers. Citibank said this month that it would let borrowers on the brink of foreclosure stay at their homes for six months, whether or not they make payments, if they turn over their property deed.

Such policies may partly reflect the fact that lenders can't keep up with all the foreclosures, some say.

"The mortgage lenders are so backlogged that some people are able to slip through the cracks," said Kathryn Davis, a real estate agent at America's Real Estate Advocates in Corona.

That was apparently the case for the Harrisons, who were told at various times that their house had been sold, that it belonged to someone else and that it was empty.

"It's been frustrating, a real major pain in the buttocks," said Eugene Harrison, a nondenominational minister with a clipped mustache and a sudden laugh.

The Harrisons missed their first payment in October 2008, shortly after Patricia Harrison, 57, lost her job as a healthcare aide and her husband's part-time towing work dried up. They said they applied for a loan modification with Countrywide Financial (since acquired by Bank of America) but were told that they couldn't receive one until they were three months behind on their payments. So they stopped paying.

In April 2009, they received a notice warning them that their property "may be sold at a public sale," and in July, they were told their house was a bank-owned property.

he bank sent a notice by FedEx in October demanding $3,000, and when the Harrisons called to discuss this notice, they were told they had four days to vacate the house.

Panicked, they arranged to stay with family in New Mexico and started packing their things, filling their garage with boxes of books, camping equipment and art. But no one came to kick them out.

"We were afraid to leave the house, afraid the sheriff was going to come," said Patricia Harrison, an amateur painter.

After contacting consumer advocates about their situation, the Harrisons decided to stay put. Soon after, two men in a white pickup truck showed up at the house and peeped in the windows, telling the Harrisons that they thought the house was abandoned.

The Harrisons suspected they were planning to move in themselves and chased them away.

The couple don't want to leave but are in the midst of a running dispute with Bank of America about the terms of their loan modification. The bank says it mailed them documents this month.

As they wade through the red tape, the Harrisons can't imagine abandoning a house where they've left their mark in the goldenrod and potpourri rose walls, the new fixtures and stenciling in the bathrooms, the fruit trees planted in the yard.

Although the Harrisons' future is uncertain, industry observers agree that the rent-free life can't last forever. As home values climb, banks will find it financially advantageous to foreclose on delinquent borrowers and sell their properties.

"In many cases, particularly in California, people owe a boatload of payments, and no bank is going to forgive that," said Guy Cecala, editor of Inside Mortgage Finance, a trade publication.

In Diamond Bar, the Fraguere family is finally moving on after living rent-free for 18 months. Job loss and other setbacks prevented them from paying their mortgage, but they say they didn't hear anything from the bank, First Franklin, until a real estate agent showed up at their door last month saying she was going to sell their house.

Sandy Fraguere wasn't surprised that it had taken the bank so long to ask them to move.

"I don't think they really knew what was going on or who was there," she said.

Next stop for the Fragueres is a hotel, where they plan to stay for two weeks until their apartment in Chino Hills is ready for them to move in. Their dogs are being boarded and their belongings stored until they can retrieve them someday. Their children, ages 8 and 9, are being steeled for more instability.

The Fragueres have started saying goodbye to their neighbors, adding yet another empty house to a block that has already seen two other families forced to pack up and leave.