House hunting? It's not a buyer's market everywhere

Potential buyers visit a home in Eagle Rock. In desirable areas, bidding wars are common.

The median price in Southern California may have plummeted, but in more desirable neighborhoods, home buyers are still engaging in bidding wars.

By Chip Jacobs / Los Angeles Times

May 2, 2009

The confident smile Sam Rivero wore as he hunted for his first house had a lot to do with the buzz thumping in his ears. Ever since home values began sinking, pundits have touted the juicy opportunities for aspiring buyers priced out of the market before, and the young business-development executive heard that cue like a sonic boom.

Out he ventured into Mount Washington, Glassell Park, Eagle Rock, Montecito Heights and other desirable middle-class communities northeast of downtown Los Angeles, searching for a bargain in the $400,000 range. Candidates came and went, and Rivero, who is getting married, was upbeat. Considering the pulverized housing values, with the median price of a Southland home today -- $250,000 -- at half of its 2007 level, the properties should come gift-wrapped, right?

As the Glendale resident and his fiancee, a makeup artist for the television show "Entourage," discovered, the supposedly wondrous buyers' market seems more consumer myth than easy pickings.

They bid $50,000 over asking price for a "great" four-bedroom contemporary in Valley Village, only to lose out to one of the 16 other offers tendered, Rivero, 33, said. A North Hollywood house he had been eager to see attracted so many people walking around with sales fliers that he couldn't find parking and drove off from the "vultures" who got there first.

"Every open house I've been to has been a zoo," said Rivero, who has examined 35 properties during the last three months. "If you follow what the [general] media say, you'd think sellers are desperate to sell a house, but when you get there it's totally the opposite."

So what's going on?

Real estate brokers and investors say would-be buyers misunderstand how the drop in housing prices has affected desirable neighborhoods. Just because an abandoned house in a troubled part of San Bernardino County might be going for $200,000, it doesn't mean you can get a nice place in Sherman Oaks for that amount -- or even twice that amount.

House hunters are trying to pounce on deals from sellers they expected to be frantic -- if not curled in the fetal position. What they're finding instead are bidding wars as low interest rates and pent-up demand in traditionally stable or chic areas have kept prices up -- not as high as the market's peak, but not nearly as low as they had hoped.

"The biggest problem," said agent Phyllis Harb, "is that people are overreacting to housing statistics, thinking they can come in and make an offer 20% below price."

As sales figures and home buyers' anecdotes are underscoring, when the residential real estate bubble burst, it set off several distinct sprays that created false hopes and confusion.

Though nearly 20,000 homes in Southern California sold in March, a 52% jump from a year earlier, a sizable number of those transactions occurred in Riverside and San Bernardino counties, where foreclosures exploded. In the region overall, foreclosure sales accounted for 55% of March's deals.

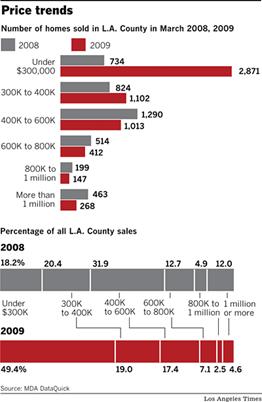

Bank-owned or not, the cheaper properties are dominating the sellers' block in the notoriously expensive L.A. County real estate market. In March, 2,871 homes under $300,000 were sold compared with only 734 a year earlier, according to real estate information firm MDA DataQuick.

At the higher end, just 202 homes priced above $1.2 million changed hands last month, compared with 354 in March 2008.

Houses priced from $400,000 to $800,000 represented less than a quarter of the market in March, down from about 45%, meaning fewer offerings for would-be buyers in that mid-market or pickier sellers, according to DataQuick.

Mark down Nicky and Bunny DeMarinis as frustrated. They offered about $1 million for a 3,300-square-foot traditional in the Los Feliz area. Though it boasted a magnificent view, the house was an ode to passe, with cheesy frescoes, gold trimming and 1970s-era kitchen appliances, they said. For all the updating it required, the owner came down only a fraction from his $1.7-million asking price and passed on the DeMarinises.

The couple, who own Nicky D's Wood-Fired Pizza in Silver Lake, have seen about 50 houses so far. They don't know where to vent their anger: lenders demanding higher down payments and less-favorable terms, talking heads distorting the market with oversimplifications or listing agents itching for bidding wars.

"You get out there and think you can grab something at a fantastic price, but that's not the case," Bunny DeMarinis said. "Each time we look at a house and see these inflated prices and our offer is rejected, we feel rejected too. We had an unrealistic portrait of what was really happening. It's disillusioning."

It's becoming a populist theme among potential local buyers and a contentious topic on websites devoted to the post-bubble market.

Jose Mares, 38, a Huntington Park police officer, said he'd been searching for eight years for a house. To him, the dark-shingled house needed too much renovation to justify the tab. He thinks he knows why it's priced where it is: There's not a glut of quality competition close by, and the owner and listing agent know their edge.

"Some want to charge $550,000 for a starter house," Mares said.

King, the agent, said she'd heard earfuls about that, and noted that this was not your father's housing crash. Today, everyone is savvier, able to analyze properties with a few keystrokes or see a street view using Google.

Instant information, though, also means fiercer competition and fewer hidden gems. As an example, King cited a 1,625-square-foot, midcentury-style fixer-upper in La Crescenta priced at $299,000. Forty people were standing on the front lawn within an hour of its listing, she said. Ultimately, there were 80 bids, 15 of them exceeding $400,000. The winning bid was $480,000.

"What I'm seeing is that perceived bargains are going in multiple offers for more than the asking, and buyers are very disappointed," King said. "Real estate is hyperlocal, so a [regional] $250,000 median price is meaningless here."

Predicting where values are headed is hardly a science either, no matter what the cable-TV experts or the galaxy of websites with every imaginable statistic say. For one thing, people selling costlier homes tend to have deep pockets buffering them from needing a fire sale to stay afloat. If they don't like the bids, they can pull their property off the market.

Banks are an even bigger X factor, and not just because of their stricter lending requirements and bailout havoc. USC real estate professor Tracey Seslen said she'd heard that lenders were carefully timing the release of homes they'd repossessed to avoid further flooding the market and driving prices down more. Those institutions also know that a fresh avalanche of foreclosures from people with resetting loans may be looming.