It’s down for first time in four years, reports say

Wednesday, May 19, 2010

San Diego County may have passed the peak in the distressed housing market, as the mortgage delinquency rate dropped for the first time in four years, new reports showed Wednesday.

The Mortgage Bankers Association said mortgage payments at least 30 days late nationally dropped one percentage point to 9.4 percent from the first quarter, while still leaving 4.4 million mortgages in technical default. California’s rate dropped from 11.3 percent to 10.9 percent and 629,000 owners late.

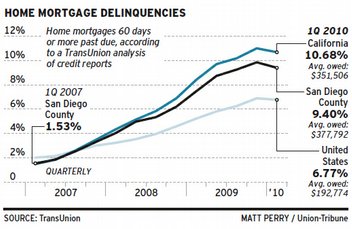

TransUnion, a credit-reporting agency, reported a similar dip, adding that California and San Diego were off the peak at the end of last year. In the first quarter, loans that were 60 days or more late in the state dropped from 11 percent to 10.7 percent. San Diego delinquencies were down from 9.9 percent to 9.4 percent over the same period, the first such decline since the rate began rising in 2006.

And Fitch Ratings reported San Diego delinquencies at 11.9 percent, unchanged from March to April, the first time there has been no increase since delinquencies starting rising four years ago.

“The patient is still in critical condition, but stable, and doctors are now working to get him back to health and move him out of ICU and into a private room,” said Rick Sharga, vice president of RealtyTrac, an Irvine company that monitors the distressed housing market.

Economists look closely at the delinquency rate because it signals whether homeowners are running into financial trouble, since a mortgage payment is usually the last bill households want to miss. Once they have fallen behind several months in a row, it becomes almost impossible to catch up, and they eventually receive a formal default notice and then fall into foreclosure.

For San Diego and most other places, delinquencies used to be almost unheard of. In 2006, the 60-day-late rate was 0.1 percent, Fitch’s figures show. By the end of 2007, when the subprime market was collapsing, the rate had crept up to 0.9 percent. But then it accelerated as the unemployment rate skyrocketed and home prices plunged.

F.J. Guarrera, TransUnion vice president of financial services, called the pullback from the peak delinquency rate good news for consumers, bankers and the economic recovery.

“With prices beginning to rise, increasing consumer confidence and positive trends in the equity markets, homeowners who are currently upside down on their mortgages might be less inclined to join the ranks of the defaulters, which have been growing in number since the summer of 2006,” Guarrera said.

He said delinquency rates are still worse than desired, but the turnaround “is a sign that things could be potentially improving in California.”

Norm Miller, vice president at CoStar Group, which collects and analyzes real estate data, said he expects loan modifications to give way to more short sales and foreclosures — a situation that would likely keep home prices from rising in the most troubled neighborhoods.

“All this points to a slow recovery with lots of foreclosures to yet work through the system,” he said. “By the time we do work through it all, interest rates, now very low, could start moving up.”

RealtyTrac’s Sharga called the current market “fairly tenuous” because a rise in joblessness, unemployment claims and housing construction could precipitate another downturn. He estimated a 55-month backlog of distressed properties needing to be resold.

But he said the nature of the inventory locally is changing from low-cost starter homes to higher-priced properties.

“You’re moving upscale into more expensive homes and a second wave of foreclosures,” he said.

For San Diego, however, Sharga said the situation is not as bleak as elsewhere, because it was not as overbuilt. Although conditions could vary by neighborhood, he said, overall, the housing crisis might be easing.